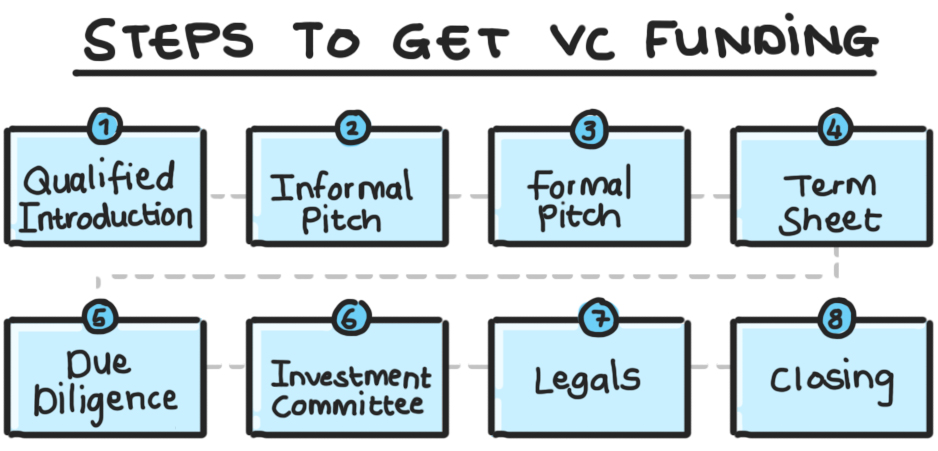

4Di Capital is a Silicon Valley-style venture capital firm in Cape Town investing in early stage technology startups. Their portfolio showcases companies like HealthQ Technologies, Impression Works and Snapt. We spoke to Co-Founder and Managing Director, Justin Stanford, who gave us the low-down on how early stage startups can pitch their business ideas to have a good chance at receiving funding. Justin described the process of securing in these eight steps:

1. Qualified Introduction: How to make the first partner contact

The best way to make the initial contact with a VC fund is through a qualified introduction to one of the General Partners (GP); either in person (e.g. at an event) or via email. Like many top-tier VCs, 4Di’s five partners rely heavily on social proofing through their networks to filter incoming proposals. “We don’t tend to look at cold call stuff at all,” Justin explains. “In fact, we have almost never invested in anything that has come out of nowhere.” That’s why startup founders who are looking for funding have to make sure to be introduced by someone the VC knows and respects. This acts as a first test.

Why?

Getting a qualified introduction is important: The nature of the Venture Capital business - which is essentially handing out money - attracts a plethora of proposals every year; too many for the GPs to deal with. More often than not, VC firms don’t publish their contact details online for exactly this reason.

What to do

Making the effort to get a qualified introduction also shows that you have spent time figuring out whether your startup is suitable for a particular investor. To ensure that you have a good understanding of the firm and the people involved, be sure to have the answers to the questions below (we’re using 4Di as an example). This avoids wasting both sides’ time and is a good first test that a lot of people simply fail at:

-

Who are they? 4Di is an independent VC fund specialising in high-growth technology venture opportunities with international ambitions, principally in the early funding stages.

-

Who are the people? 4Di has five partners: Anton van Vlaanderen, Douglas Cherry, Erik van Vlaanderen, Justin Stanford and Laurie Olivier.

-

What do they actually look for? 4Di are looking for founder teams who show “hungry passion, commitment, domain expertise and deep insights into the large market problems” in the way they tackle technology solutions.

-

What is their mandate? The fund’s mandate includes early- and growth-stage investments. It focuses on scalable technology opportunities in the FinTech, InsurTech and HealthTech verticals and particularly on those with ambitions to reach international markets.

2. First meeting: How to successfully pitch your business idea

If the qualified introduction has been successful, the next step is a first meeting with the partner you approached and maybe another GP from the fund. This is an informal pitching session and acts as a filtering meeting. The partner(s) will decide afterwards whether they want to champion your startup internally or not.

To determine this, they will do a general check of the following:

- Does the fund have a mandate for this kind of business?

- Is there an opportunity? Does it have high gross margins, potential to reach break-even cash flow within 12 to 36 months, potential for residual income and a low level of liability?

- Is there a market, e.g. is there a demand for the problem solution?

- Does the product make sense and solve a real problem?

How to prep

A simple way to make sure that the pitch is covering all the necessary buckets is to look at examples of other great pitch decks. People often fail to cover the bases, e.g. addressing each of the different areas and within those, sticking to a tight focus. Justin recommends this pitch deck from Crowdfunder as a good example to follow. It covers all essential topics in 12 simple slides:

- Elevator Pitch

- Momentum, Traction, Expertise: Your key numbers

- Market Opportunity: Define market size & your customer base

- Problem & Current Solutions: What need do you fill? What other solutions are out there?

- Product or Service: Explaining your solution

- Business Model: Key Revenue Streams

- Market Approach & Strategy: How you grow your business

Team & Key Stakeholders (Investors, Advisors) - Competition

- Investment: Your ‘Ask’ for funding, Basic use of funds

- Current Financials

In Justin’s experience, good competitive analyses and the outlines of the current financials are almost always missing or disproportionately weighted - a good point to note in order to stand out.

Why?

It’s important to realise that the 12 key points above relate to the key questions in an investor’s mind. They all have to be addressed on a high level - too much detail and time spent on one aspect is just as disadvantageous as leaving out one of the key points: “A lot of people don’t do the research and don’t cover all the buckets,” Justin notes.

“I’ve seen pitches that wander all over the place and go into too much detail. All you’re trying to do is captivate someone’s interest and start a conversation.”

He advises that - maybe counterintuitively - pitches shouldn’t go into too much depth on the financials: “People sometimes put up spreadsheet tables. You can’t get those at a glance.” As a founder, rather give VCs a rough idea of your burn and spend on salaries to allow them to compare these to the usual.

The outcome

Especially if they are interested in your business, the VC will often give the startup founder concrete feedback on the pitch. “Sometimes I’ll even say: ‘Here are the improvements you should make. Send me your deck before the formal pitch’,” Justin says.

3. Second meeting: formal pitch to the entire VC team

The first formal pitch with all the partners allows the funding team to assess whether the startup fits their mandate, judge the startup founders’ commitment and identify potential red flags. “First, I think we try and interrogate the opportunity, the industry and the people to get a sense of their insights,” Justin says.

What happens?

Based on the (updated) pitch deck, the VCs will ask specific questions: How did the founders arrive at their problem statement? Are they dealing with an issue they have themselves or are they trying to solve external problems? “Solvers of internal problems have often been the strongest people coming out of the trenches,” he explains.

Mandate

One important question is that of the mandate fit. According to Justin, this is an often misunderstood aspect of a VC’s decision making process: A fund is building a certain portfolio of “buckets” of different industries. The portfolio dynamics need to be carefully balanced so that the company in question has to:

- fit into one of those areas and bring some innovation with it and

- be scalable enough, meaning have at least 100x potential.

If the startup doesn’t fit the mandate, it doesn’t mean it’s a bad business, it just means it’s not a good fit for a particular fund at a specific time: “There’s a number of constraints we are looking at,” Justin says. “Maybe we’re heavily loaded on high risk and now want a bit lower risk, for example.” The economic numbers need to return in aggregate and that’s why the VCs need to look at their other investments and how the new commitment would slot into them.

Commitment

In addition, they will look into how much of their own cash the founders have invested in the business. “This is a big, big key for us,” Justin says. “The more founder commitment, the better because it shows tighter alignment and strong belief.” Sometimes however, he also sees too much money invested in something - a red flag because the founders have spent a lot but only delivered X. “We like lean burn startups for obvious reasons.”

Red Flags

Another important question the VCs are trying to answer is whether the team are realistic about the obstacles they might face. “I’ll blatantly ask: ‘Who are your competitors? What are the problems? What’s going to make the business fail?’”

Most people fail at this very point because they haven’t researched it that deeply.

Startup teams are often so focused on the potential and their own journey that they haven’t stopped to look at other people’s journeys to learn from them.

The outcome

After the formal pitch, the VC-team will have a funding discussion: “We say to ourselves: ‘Okay, assuming the people, opportunity and product check out - Would it solve the various fund concerns?’” Here, the 4Di team is doing sanity checks on return, risk, geographic and political exposure as well as markets.

If these discussions result in a positive consensus, the championing partner will have further discussions with the founders and does a few more checks. Then the term sheet offer discussions begin.

4. Sketching out terms and amounts: The term sheet

The term sheet (also called Memorandum of Understanding (MOU) or Heads of Agreement) sketches out the terms and amounts of a potential investment. “It says: ‘At face value, we like everything we hear and see,;” Justin explains. The term sheet is a non-binding offer that is subject to due diligence - a drafting process that, according to Justin, often requires “a lot of jiggering and Tetris”.

The VC has now done a basic assessment of how much money they think the company needs, how big their round size should be and how much of that round they are willing to take on. Sometimes they will take it all and sometimes they will send the startup founders off to find the rest with external investors. The rule of thumb is that typical rounds dilute a company about 20% to 30%. “How we move that line is somewhat of a risk adjuster,” Justin says. The partners look at realistic returns, where the business currently lies on the risk spectrum and whether they need to own a bit more or a bit less to get to the necessary fund economics.

What is it?

“What you are actually trying to do here is to find each other before you put too much work into the deal,” Justin says. If the two sides can’t agree, they can just walk away.

That’s why the term sheet is a fairly detailed document of five to six pages that 4Di drafts based on the National Venture Capital Association (NVCA) standard template. In it, they are trying to balance a variety of risks (like the founder leaving), design terms that engineer alignment and lay out things like the cap table.

What happens?

Again, this process requires a consensus. The champion partner meets with founders to discuss and explain the term sheet, and do the necessary panel beating to create alignment. Sometimes, this even means that the founding team has to be reshuffled. “I’m sitting in a situation right now where there was a gap in the team,” Justin says. “They then went and found a brilliant person, equity got sorted and boom, now we decided it’s investible.”

The term sheet is the basis on which a due diligence (DD) and, ultimately, a deal can be done. This negotiation alone can take a month, especially if the startup side involves a lawyer. The document is not binding other than that, once signed, it gives an exclusivity or “no shop” period of 90 days. In those three months, the company is prohibited from negotiating with other parties whilst the investor puts in time and effort to:

- Perform the due diligence

- modify the term sheet

- build an internal investment hypothesis (see point 5)

- get approval from the Investment Committee (IC)

- take the deal to the lawyers and

- sign the deal.

5. Due diligence

After the two sides have reached a principle agreement on the terms, they start to work on a formal deal. This is not run by the champion partner because the person who brings the deal in runs the risk of falling in love with the project they are championing. At 4Di, the DD is normally run by Charlotte Koep, who happens to be a lawyer, together with another partner. For this, they need to complete two jobs: ticking off all the checklist points and creating the internal investment hypothesis document.

Ticking off the checklist

“We can’t just willy-nilly write checks. We’ve got to follow due process, cover all the bases or else we could get ourselves into trouble,” Justin says. This is something they do together with the founders. In a process of about two weeks (that is part of their fiduciary duty as investment managers), the VCs do a thorough check on outstanding matters.

They visit the company on site and meet everyone they haven’t met yet, like the staff and other investors or partners and interrogate references and customers. They are trying to answer the questions:

- Why do people like their product?

- Why did someone choose it over another one?

- What are the obstacles and problems?

The VCs will also take a look at all the financials and legal background to identify any red flags like outstanding taxes, conflicts of interest or legal battles (are they being sued by anyone?). Depending on the answers to any of the above questions, the standing term sheet might be subjected to minor modifications. Equity, value or term changes are a common element of the due diligence process when VCs uncover unforeseen additional risks. “There’s always something, some small problem typically,” Justin says. “Only if you find really big red flags in the market you might bail out on the deal completely.”

Investment hypothesis

“As a fund, we’ve got an actual written mandate which says this is what you will invest in and these are the requirements for an investment,” Justin explains. The investment hypothesis document has to meet these criteria. The resulting document has to be a rational, sober viewpoint of the total picture, including realistic risks and problems. “We will build a case on why the opportunity is good, why we like the team, what their strengths and weaknesses are,” he says.

Outcome

The outcome of this process is an adapted, agreed upon term sheet and a document consisting of two parts - the completed checklist and the investment hypothesis. Despite it being and staying an internal document, it has to be on file so that it can be consulted to check on the original reasons and concerns around the investment. The real audience will be the investment committee which is where the final decision is being made.

6. Investment Committee

The Investment Committee meeting is where the fund, based on the presented TS and DD, decides on whether or not to offer the startup money. Some of the partners on the committee are seeing the deal for the very first time now. Even the champion partner might be confronted with some fresh challenges because they didn’t run the DD.

At 4Di, the IC consists of all five partners. The fund sometimes invites representatives of their Limited Partners, meaning investors, to sit in as observers. The LPs don’t have a vote and are just there to counterbalance - listen and challenge a few things, ask a few tough questions. “We are managing stakeholders as well, so we want people to agree with our decision and back us,” Justin says.

What happens?

The IC discussion is designed to be robust and difficult. Based on the very equally weighed DD that realistically expands both on the strengths and weaknesses of the business idea, the decision to invest has to be made despite or in light of the risks outlined.

“That’s how you make a very sober investment decision that you can back,” Justin explains. 4Di makes this decision based on full consensus and then takes the TS to the lawyers.

7. Legals

The TS forms the basis for the lawyers’ briefing. They will take it and draft the full-length agreement, also called “Long Form”. This goes back and forth between the different parties: “Everyone gets to look and comment and then the closing is when it all gets signed and the cash flows,” Justin says.

8. Closing

After everything is signed, the money transfer happens according to the stated agreements - cash usually flows quite fast after the closing.